Drug development has long been defined by its brutal economics: an average of 10 to 15 years from target identification to patient access, with a failure rate exceeding 90% in clinical trials and per-drug costs routinely crossing $2 billion. These constraints have not disappeared, but artificial intelligence is beginning to compress them in ways that were difficult to model even five years ago. The industry is no longer asking whether AI has a role in drug discovery. The question now is how quickly organisations can build the infrastructure, data governance, and regulatory fluency to extract durable value from it.

Molecule screening and target discovery: the earliest gains

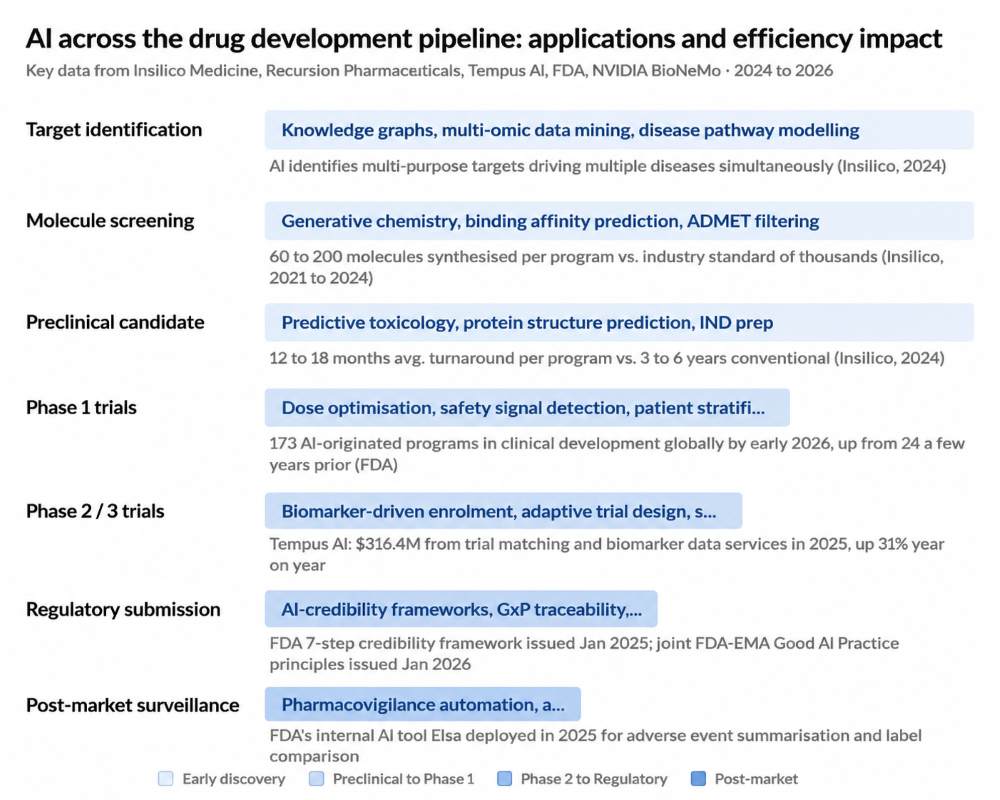

The first commercially significant applications of AI in life sciences emerged in computational chemistry and structural biology. Machine learning models capable of predicting molecular binding affinity, protein folding, and ADMET properties gave medicinal chemists a way to filter vast chemical libraries before any compound entered a lab. What previously required synthesising and testing hundreds of thousands of molecules can now be narrowed computationally.

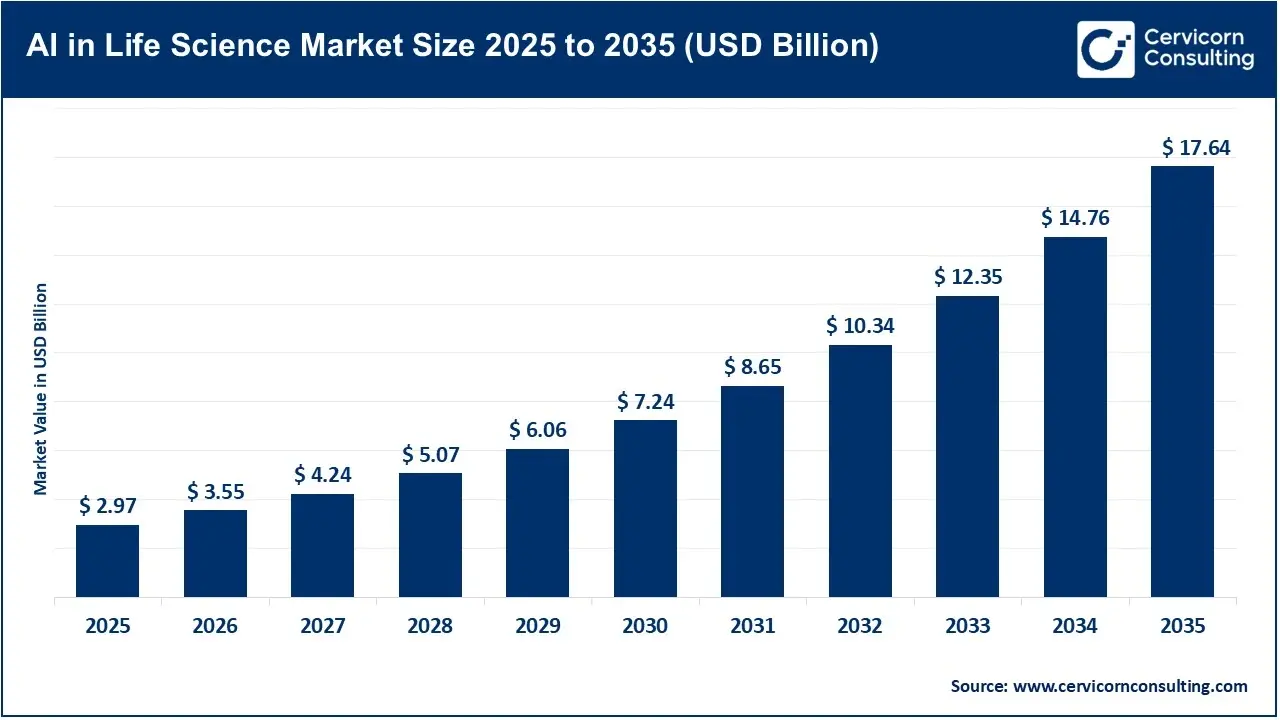

“According to Cervicorn Consulting, the global AI in life science market size was valued at USD 2.97 billion in 2025 and is projected to surpass USD 17.64 billion by 2035, expanding at a CAGR of 19.5% from 2026 to 2035. This rapid growth reflects increasing pharmaceutical investment in AI-led drug discovery, predictive analytics, clinical trial optimisation, and regulatory automation as the industry shifts toward data-centric R&D models.”

The scale of industry commitment was underscored in March 2026 when Insilico Medicine signed a collaboration with Eli Lilly worth up to $2.75 billion, including $115 million upfront, granting Lilly exclusive worldwide rights to a preclinical portfolio discovered using Insilico’s Pharma.AI platform. Between 2021 and 2024, Insilico nominated 20 preclinical candidates with an average turnaround of 12 to 18 months per program, compared to three to six years in conventional discovery, while synthesising only 60 to 200 molecules per program. The company’s lead asset, rentosertib, went from project start to Phase 1 in under 30 months.

“The industry is moving from AI-assisted science to AI-native pipelines, and this partnership reflects that shift.” Alex Zhavoronkov, founder and CEO, Insilico Medicine

Clinical trial optimization and biomarker intelligence

Patient recruitment, protocol design, and site selection consume a disproportionate share of clinical development budgets. AI-driven trial matching platforms are now being deployed to identify eligible patients through real-world data, reducing enrolment timelines that historically stretch to 30% of total trial duration. Tempus AI, which reported $1.27 billion in revenue for 2025, an 83% year-over-year increase, has built its commercial model around exactly this use case. Its data and applications segment, which generated $316.4 million in 2025, licenses de-identified genomic and clinical datasets to pharma partners for trial matching, biomarker discovery, and contract research operations.

Biomarker identification, one of the more technically demanding tasks in precision oncology, is another area seeing structured AI integration. The ability to stratify patient populations by genomic signature before trial initiation improves the probability of clinical success and reduces late-stage attrition, historically the most expensive point of failure in drug development.

Genomics, precision medicine, and predictive toxicology

Multi-omic data integration, combining genomic, transcriptomic, proteomic, and clinical datasets, has created an analytical surface that far exceeds what traditional bioinformatics could process. AI models trained on these layered datasets are now identifying disease subtypes, resistance mechanisms, and patient segments that were previously invisible to clinical investigators.

Predictive toxicology is emerging as one of the more commercially impactful applications. Early computational identification of hepatotoxic or cardiotoxic signals can eliminate compounds from consideration before they enter IND-enabling studies, potentially saving years of work and tens of millions in preclinical spend. Recursion Pharmaceuticals, which in 2025 open-sourced Boltz-2, a billion-parameter generative model for protein structure prediction and ligand binding developed with MIT and NVIDIA, reported the model was downloaded by more than 40,000 users within weeks of release.

Lab automation and the wet-dry continuum

At the J.P. Morgan Healthcare Conference in January 2026, NVIDIA announced a major expansion of its BioNeMo platform, described as an open development environment enabling lab-in-the-loop workflows for AI-driven biology and drug discovery. Simultaneously, Eli Lilly and NVIDIA announced a co-innovation lab in the Bay Area backed by over $1 billion in committed investment over five years, focused on accelerated, closed-loop discovery and AI models for clinical development. NVIDIA also announced a collaboration with Thermo Fisher Scientific to build autonomous laboratory infrastructure, extending AI from computational prediction into physical lab execution.

The convergence of robotic lab automation, AI model inference, and real-time data feedback loops is enabling what researchers call the wet-dry continuum: a closed system where

computational predictions are tested physically, results are fed back into models, and the next synthesis round is informed by the previous cycle’s outcome.

Market perspective: capital flows and commercialisation

Venture investment in AI-first drug companies reached approximately $11 billion across 348 rounds in 2025, up from $8.9 billion in 2024, according to DealForma data. 2025 also saw 22 deals exceeding $100 million in healthcare AI, more than any prior year and significantly more than any other AI vertical. In Q1 2026 alone, AI biotech startups raised several hundred million dollars in notable rounds. According to expert analysis, 168 new strategic alliances in pharma involving AI were signed in 2025, reflecting the pace of corporate adoption beyond venture-stage investment.

Analyst forecasts suggest that up to 27% of pharma R and D spending could be influenced by AI by 2035. Large pharma companies increasingly view AI infrastructure, covering compute, data, and model development, as core R and D expenditure rather than experimental technology spend. The pattern across Lilly, AstraZeneca, Pfizer, GSK, and Sanofi points toward a structural shift in how discovery pipelines are resourced.

Regulatory and compliance: the framework takes shape

Regulatory ambiguity has been the most frequently cited constraint on AI adoption in life sciences. That position has shifted materially over the past 18 months.

| Regulatory Body / Initiative | Key Highlights | Market Impact / Significance |

| U.S. Food and Drug Administration Draft Guidance | Introduced a 7-step credibility assessment framework for evaluating AI in regulatory decision-making. Established the CDER AI Council and launched Elsa, an internal generative AI tool for adverse event summarization. Final guidance is expected in Q2 2026. | Strengthens regulatory clarity for AI adoption in drug development, improving trust, compliance, and validation requirements for pharmaceutical companies. |

| U.S. Food and Drug Administration & European Medicines Agency Joint Principles | Released 10 guiding principles for Good AI Practice (GAIP) across the full pharmaceutical product lifecycle, covering early research, clinical trials, manufacturing, and post-market surveillance. These principles are currently non-binding. | Signals the upcoming global regulatory framework for AI-driven drug development and encourages early compliance preparation among pharma firms. |

| European Medicines Agency AI Work Plan | A five-year strategic AI framework focused on integrating AI into discovery, clinical development, manufacturing, and lifecycle monitoring. Under the European Union AI Act, pharmaceutical AI systems in quality control are categorized as high-risk. | Increases demand for robust risk assessment, explainability, and human oversight, impacting AI deployment costs and compliance strategies. |

| GxP & Data Integrity Framework | Requires full documentation of every AI processing step, including model validation, dataset traceability, and analytical decisions in compliance with GxP standards. Data provenance and auditability have become key regulatory expectations. | Enhances focus on transparency, audit-readiness, and data integrity, driving investment in compliant AI infrastructure and validation systems. |

By early 2026, AI-originated drug programs in clinical development had surpassed 173 globally, up from approximately 24 only a few years prior. The FDA’s posture has shifted from passive observation to active framework-building, including an Accelerated AI Pathway Pilot for Phase I programs.

Future outlook

The near-term priorities for the industry are predictable: integrating AI-derived insights into regulatory submissions in formats that satisfy emerging FDA and EMA expectations; building proprietary data assets of sufficient scale and quality to train differentiated models; and closing the talent gap between computational biology capability and traditional drug development expertise.

The medium-term picture is more structurally significant. If AI can consistently reduce preclinical attrition rates and improve patient stratification in Phase 2 trials, where the bulk of drug development value is either created or destroyed, the economics of the entire industry shift. Smaller organisations with proprietary biological datasets but limited synthesis capacity would become more competitive. The cost of maintaining a broad pipeline falls. The ability to prosecute rare disease indications, where patient populations are small and traditional trial economics are prohibitive, improves substantially.

There are cautions worth noting. Recursion’s lead AI-derived candidate REC-994 missed its Phase 2 endpoint, illustrating that AI-generated hypotheses must still survive the biological complexity of human disease. Clinical success rates, even for AI-discovered compounds, will not approach 100%. The value of AI in drug development is probabilistic improvement at population scale, not elimination of individual program risk.

The structural argument for AI in life sciences is now largely settled at the executive level. What remains contested is execution: which platforms produce durable competitive advantage, which data assets are genuinely proprietary, and which regulatory frameworks will govern the field as AI-generated evidence becomes a routine component of drug submissions. The organisations building disciplined answers to those questions are likely to define what AI-native pharmaceutical development looks like by 2030.

The $2.75 billion Lilly-Insilico deal and the $1 billion Lilly-NVIDIA co-innovation lab are not endpoints. They are early structural signals of an industry reconfiguring its R and D infrastructure around computational biology, with consequences for timelines, economics, and ultimately patient outcomes that will take the rest of this decade to fully measure.

For deeper market intelligence on AI-driven biotechnology trends, readers can explore industry research and analysis from Cervicorn Consulting.